PwC Working Document on FSV Effects: Hard Evidence of Institutional Racism in the Tax and Customs Administration

Document Details

| Field | Content |

|---|---|

| Source Document | PwC, “Onderzoek effecten FSV, Voorbeeld casussen, Werkdocument” (Investigation into FSV Effects, Sample Cases, Working Document) |

| Date | 9 February 2022 |

| Classification | CONFIDENTIAL (VERTROUWELIJK) |

| Author | PwC (PricewaterhouseCoopers) |

| Commissioned by | Belastingdienst (Tax and Customs Administration) |

Summary

The confidential PwC working document, dated 9 February 2022, provides hard evidence of institutional racism at every level of the Tax and Customs Administration. The document describes how “allochtoon” (non-native) served as the first selection criterion for starter visits, how “stoppertjes” (stoppers) as an institutionalised practice led to benefits terminations without due process and how nationality, surname and religion were used as formal risk indicators. The document also reveals the scale of internal investigations: 36.7 million files across 106 locations, totalling 8.9 terabytes of data, of which only a fraction was provided to the House of Representatives.

Part 1: Institutional Racism at Every Level

1.1 Toeslagen (Benefits Division)

Within the Benefits Division, risk profiles were constructed in which ethnic characteristics played an explicit role. Citizens with a migration background were classified as suspicious more frequently and more rapidly. The selection criteria were not based on objective financial behaviour but on demographic characteristics.

1.2 Particulieren (Individuals Division)

The Individuals Division applied comparable ethnic profiling criteria in the assessment of tax returns. Signals were followed up more frequently and more strictly when the individual concerned had a migration background.

1.3 MKB (SME Division)

Within the SME Division, entrepreneurs with a migration background were systematically selected for further investigation more often. This applied in particular to gastouderbureaus (childcare agencies) and entrepreneurs in the informal economy.

1.4 De Poort (The Gate)

The Gate division, responsible for the central coordination of inspections, explicitly used nationality in query instructions for analysts. This means that nationality was embedded as a search criterion in the formal work processes.

Part 2: Discriminatory Selection Criteria

2.1 “Allochtoon” (Non-Native) as First Selection Criterion for Starter Visits

The PwC document establishes that “allochtoon” served as the very first selection criterion in determining which new business starters received an inspection visit. This constitutes direct evidence of ethnic profiling at the core of operational practice:

The term “allochtoon” functioned as the primary filter before any financial investigation was conducted.

2.2 Surname Ending in “…IC” as a Risk Indicator

Analysts at De Poort used the surname of individuals as a risk indicator. In particular, surnames ending in “…IC” (a patronymic common among persons of Balkan or Eastern European descent) were classified as elevated risk.

This practice means that citizens were selected for fraud investigation solely on the basis of their name, without any substantive grounds.

2.3 “Mosques” as a Standard Risk in Formal Manuals

“Mosques” were included as a standard risk category in the formal manuals of the Tax Administration. This means:

- Religious identity was associated with elevated fraud risk

- The association was institutionalised in formal documentation

- ANBI status (Algemeen Nut Beogende Instelling / Public Benefit Organisation) for mosques was systematically scrutinised more strictly

2.4 Nationality in Query Instructions

At De Poort, query instructions for analysts were drafted in which nationality was an explicit search criterion. This means that the ICT systems of the Tax Administration were used to filter citizens on the basis of their nationality, a practice that contravenes the prohibition of discrimination under Article 1 of the Dutch Constitution and Article 14 of the ECHR.

Part 3: “Het Stoppertje” (The Stopper), Institutionalised Due Process Violation

3.1 The Practice

The “stoppertje” was an institutionalised practice whereby:

- A Tax Administration employee included a codeword in a message

- The message was sent to the Benefits division

- On the basis of this single message, the citizen’s benefits were terminated

- No due process followed, no hearing, no adversarial proceedings, no reasoned decision

3.2 The Scale

The PwC document reports that 160 sent messages containing the codeword resulted in a benefits termination. This concerns 160 cases in which citizens lost their income without any form of legal protection.

3.3 The Legal Consequence

The stoppertje practice violates multiple fundamental legal principles:

- Right to be heard (Art. 7:1 GALA): Citizens were not heard before termination

- Duty to give reasons (Art. 3:46 GALA): The termination was not reasoned

- Principle of due care (Art. 3:2 GALA): No careful investigation was conducted beforehand

- Prohibition of arbitrariness: The termination was not based on objective criteria

Part 4: ANBI Footnote, Direct Evidence of Ethnic Differentiation

4.1 “***MITS NIET AUTOCHTOON” ("***PROVIDED NOT NATIVE")

The PwC document cites a footnote in the ANBI documentation (Algemeen Nut Beogende Instellingen / Public Benefit Organisations) containing the text:

***MITS NIET AUTOCHTOON

This footnote constitutes direct evidence of ethnic differentiation in the policy application of the Tax Administration. It means that ANBI status and the associated tax benefits, was assessed differently depending on the ethnic background of the applicant.

4.2 Significance

This footnote shows that discrimination was not the result of individual employee bias but was embedded in the formal documentation and policy frameworks of the Tax Administration. It constitutes a formal piece of evidence of institutionalised discrimination.

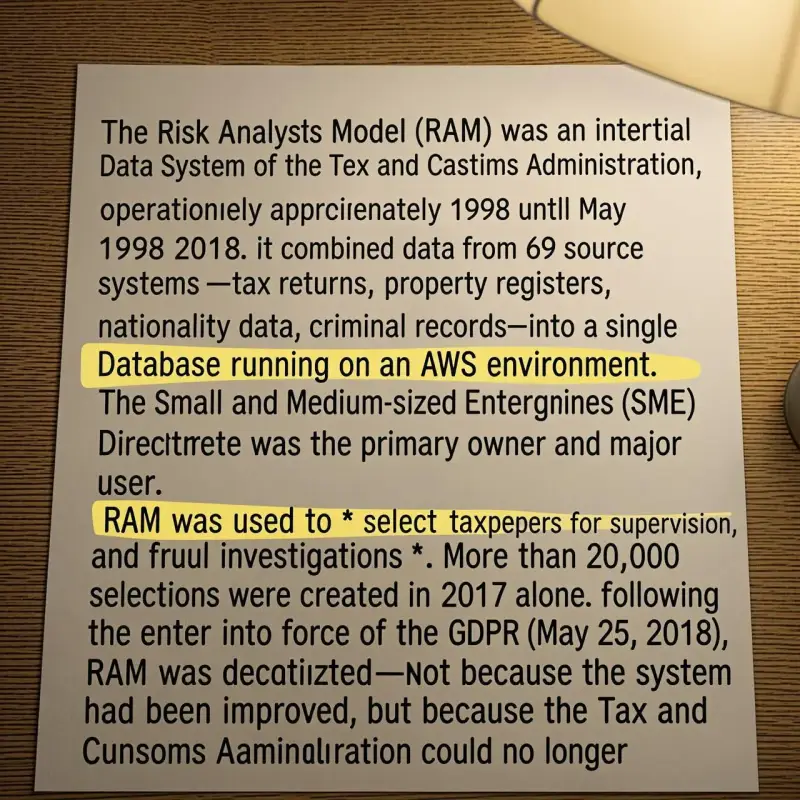

Part 5: FSV Export and Profiling

5.1 Export Without Filtering

The FSV export for profiling purposes was conducted without filtering. This means that the entire database of more than 180,000 registered citizens was used for profiling purposes, without:

- Verification of the accuracy of the registrations

- Separation between verified and unverified signals

- Assessment against the necessity and proportionality of the data processing

5.2 Consequence

The result was that 180,000 citizens, the vast majority of whom were registered without justification, were subjected to profiling by other government agencies. The FSV functioned as a stigmatisation instrument on a national scale.

Part 6: Project “Patser” (Show-off)

6.1 The Case

The PwC document describes Project “Patser” as an investigation that was initiated on the basis of:

- A person in an expensive car

- With a “conspicuous” appearance

This is a textbook example of ethnic profiling: the sole basis for the investigation was the subjective assessment of a citizen’s appearance, not any objective signal of financial misconduct or fraud.

6.2 Institutional Context

Project “Patser” is not an isolated incident. It is a manifestation of an institutional culture in which physical characteristics and ethnicity function as primary triggers for fraud investigation.

Part 7: CAF-11/Hawaii, The Scale of the Investigation

7.1 Scope

The internal investigation CAF-11/Hawaii encompassed:

| Parameter | Value |

|---|---|

| Files | 36,700,000 (36.7 million) |

| Locations | 106 |

| Data volume | 8.9 terabytes |

These figures illustrate the unprecedented scale of the internal investigation into the FSV and related systems.

7.2 Disclosure to the House of Representatives

Of the 36.7 million files, only a fraction has been provided to the House of Representatives (Tweede Kamer). This raises the question:

- What information is being withheld?

- Is there evidence of deliberate selective information provision?

- Can the House of Representatives exercise its oversight function without complete information?

Legal Frameworks and Violations

| Legislation / Principle | Violation |

|---|---|

| Article 1 Dutch Constitution (equality principle) | Discrimination on the basis of ethnicity, nationality and religion |

| Article 14 ECHR (prohibition of discrimination) | Ethnic profiling in selection criteria |

| Article 8 ECHR (private life) | Unfiltered FSV export for profiling |

| GDPR (Arts. 5, 6, 9) | Processing of personal data without legal basis |

| GALA Art. 3:2 (due care) | “Stoppertjes” without proper investigation |

| GALA Art. 7:1 (right to be heard) | Terminations without hearing |

Source References

- PwC, Onderzoek effecten FSV, Voorbeeld casussen, Werkdocument, 9 February 2022. Classification: VERTROUWELIJK (CONFIDENTIAL).

- Belastingdienst, internal documentation CAF-11/Hawaii investigation.

- Constitution of the Kingdom of the Netherlands, Article 1 (equality principle).

- European Convention on Human Rights (ECHR), Articles 8, 14.

- General Data Protection Regulation (GDPR), Articles 5, 6, 9.

- General Administrative Law Act (GALA/Awb), Articles 3:2, 3:46, 7:1.

Open Questions

- Why has the complete PwC working document not been made public?

- Which files from the CAF-11/Hawaii investigation have been withheld from the House of Representatives?

- Have the employees who sent “stoppertjes” been personally held to account?

- Was the ANBI footnote “***MITS NIET AUTOCHTOON” still in use at the time of the investigation?

- How many citizens were unjustly investigated on the basis of “Patser”-like criteria?

- Has a criminal investigation been initiated against those responsible for the institutionalised discrimination?

Document prepared on the basis of the confidential PwC working document “Onderzoek effecten FSV, Voorbeeld casussen, Werkdocument”, 9 February 2022. All quotations and statistics are derived from the source document.